The Rising Demand for Gold and Singapore’s Value Proposition

By SBMA

Gold is closely connected with the life and culture of Asia and also plays an important role among investors here. In some countries in the region, gold is even regarded as more stable than the national currency and is used as a medium of exchange and a unit of measurement.

In general, people in Asia like to buy gold jewellery, not only as accessories or gifts for cultural or religious ceremonies such as weddings, festivals, and other special occasions, but also to store their wealth. When there is a bountiful harvest, people use their excess money to buy gold, to keep it for a rainy day. People then resell their gold to jewellery shops when they need money or visit pawnshops for short-term borrowing. Besides the demand for jewellery, political and global macroeconomic uncertainties mean that many investors consider gold as a stable and reliable asset, and many of them purchase physical gold such as bars or coins as part of their investments.

The growing middle class in the past decade among the Association of Southeast Asian Nations (ASEAN) countries with more discerning taste have posted challenges to the gold jewellery industry as well. Gold jewellery can no longer only serve the purpose of store of wealth but must appeal to the lifestyle changes of the emerging younger population. The digital transformation to the wealth management industry has also impacted the retail access to gold products, witnessed both in Singapore and the region, start-up entrepreneurs enticing both younger and savvy portfolio investors to gold investing/saving through digital gold products, an ongoing process that was received positively by the regulators and young investors alike.

Asia is the main driver of the rising demand for gold globally. Asian demand for jewellery and investment totalled 2,045 tonnes in 2021.

Asia is the main driver of the rising demand for gold globally. Asian demand for jewellery and investment totalled 2,045 tonnes in 2021. The continent does not only comprise gold importing nations, but also includes countries that export gold as scrap or by-products of mining. According to Metals Focus, Asia’s gold mine production output remained the second-highest globally, at 610.4 tonnes in 2020, behind Africa at 931 tonnes.

Additionally, there is increasing investor interest to store gold in Singapore, which offers a neutral and alternate location for them to store their wealth. With its world-class physical infrastructure, Singapore is well placed to accommodate this demand. Its innate attributes of neutrality, economic and political stability, excellent connectivity and reputation as an important financial centre have long appealed to global investors. In addition, Singapore has a strong, efficient and transparent legal and judicial framework, as well as a strong rule of law. According to the Monetary Authority of Singapore (MAS), the country has the largest pool of assets under management (AUM) in Asia, with S$2.6 trillion in 2015. In 2020, its AUM increased by 17%, reaching S$4.7 trillion (US$3.5 trillion).

In addition to the Free Port at Changi Airport, Singapore also offers gold storage at The Reserve, a facility recently built by local precious metals dealer Silver Bullion. The Reserve is capable of storing up to 15,000 tonnes (about 482 million troy ounces) in silver – 60% of the annual world production – and 50 tonnes of gold.

The physical allocation of gold in investment portfolios has also been growing in Singapore, which has led to a growth in the number of companies setting up bullion operations in Singapore. Using the country as a base, they are able to leverage its infrastructure and geographical location to expand into Asia Pacific markets and benefit from the lack of foreign exchange and capital restrictions, as well as the availability of several tax incentives.

Economic overview

Singapore is a hub for logistics and finance in Southeast Asia and transacts very large imports and exports compared to the size of its own economy (Table 1). As a result, domestic economic trends are often influenced by broader economic and currency trends. Singapore also has very close connections with the Chinese economy through its extensive overseas network.

Table 1: Key Figures

| Singapore | 2021 |

|---|---|

| Population | 5.5 million |

| Economic Growth | 7.6% |

| GDP | S$ 533,352 million |

| GDP/P | S$97,798 |

| CPI | 2.3% |

| Exports | S$614.1 billion |

| Imports | S$545.9 billion |

| Foreign Reserves | U$417 billion |

| External Debt | 471.3% of GDP (2020) |

History of Singapore’s precious metals market

Since the 1960s, Singapore has been a gold distribution centre for Southeast Asia, with its gold largely sourced from London and Zurich. In 1969, in the wake of a global evolution of the free gold market and a two-tier price structure following the collapse of the London Gold Pool, Singapore established an over-the-counter (OTC) gold market.

However, from 1969 onwards, only non-residents could perform gold transactions in Singapore, and banks and bullion dealers trading gold required authorisation from the Singapore government. Beginning in 1973, Singapore residents were finally allowed to trade gold, and the gold dealer licensing requirement was abolished.

In November 1978, a group of Singaporean bullion dealing banks and brokers formed the Gold Exchange of Singapore (GES). Founder members included United Overseas Bank (UOB), N. M. Rothschild & Sons Ltd and Overseas Chinese Banking Corporation (OCBC). GES listed two physically deliverable gold futures contracts: 100 oz and 1 kg. GES also established its own clearing house, the Singapore Gold Clearing House, whose clearing members were OCBC, UOB, Overseas Union Bank (OUB), DBS Bank Ltd and the Bank of Nova Scotia. GES gold contracts saw strong initial interest but trading volumes tailed off by 1983.

GOLD INVESTMENT ACCOUNTS AND GOLD ACCUMULATION PLANS OFFER ALTERNATIVES TO BUYING PHYSICAL METAL.

In late 1983, GES was integrated into a new financial futures market – the Singapore International Monetary Exchange (SIMEX), a collaboration between GES and the International Monetary Market (IMM), a division of the Chicago Mercantile Exchange (CME). In 1984, SIMEX launched a cash-settled 100 oz gold futures contract based on loco London prices. However, this contract also saw a gradual demise in demand and activity ceased by 1996, which led to it being phased out in 1997. SIMEX then merged with the Stock Exchange of Singapore in 1999 to form the current multi-asset Singapore Exchange (SGX).

Singapore’s role as a redistribution centre for the region in physical gold reached record levels in 1992, when gold imports hit 414 tonnes (almost half of Asia’s total consumption). Since then, imports have declined as a result of market liberalisation measures adopted by some of its immediate neighbours.

Consumption by domestic jewellers had, for many years, hovered around 18–22 tonnes at saturation level. The introduction of a 3% Goods and Services Tax (GST) in 1994 softened the demand for gold products. In 2003, GST was increased to 4% and then to 5% in 2004. In 2007, it was increased further to the current level of 7%. Domestic jewellery consumption was reduced to single digit tonnes and gold bar consumption is negligible due to the GST.

The establishment of the Singapore Freeport in 2010 provided Asia with its own Fort Knox, outfitted with cutting-edge security. It is a bonded warehouse, and no GST was involved if movement is confined within the premises, hence it was a popular choice for high-net-worth investors. Located next to Singapore’s Changi International Airport, it offers 22,000 sq. metres of strong rooms and showrooms with direct access to the airport runway and armed guards around the clock.

In 2011, International Enterprise (IE) Singapore (now known as Enterprise Singapore) revisited the precious metals sector with a proposition of revitalising Singapore as a gold hub like it was before the imposition of GST in 1994. It was met with the support of the industry key stakeholders. Recognising that investment precious metals (IPM) are essentially financial assets like other actively traded financial instruments like stocks and bonds, and to facilitate the development of IPM refining and trading in Singapore, the government announced in early 2012 that IPM would be GST exempt from October 1, 2012. As a result, the volume of non-monetary gold import jumped 78% and exports increased 37% in 2013 (data from IE Singapore).

With the concerted effort of multiple government agencies, Singapore was able to quickly anchor a first-class London Bullion Market Association (LBMA) accredited gold refinery – Metalor Technologies Singapore Pte Ltd, which opened in June 2014. This has proved to be an important addition to complete the supply chain and the eco-system of the bullion trade.

At the 2014 London Bullion Market Association Bullion Market Forum in Singapore, Singapore Trade and Industry Minister Lim Hng Kiang announced the Singapore Kilobar Gold Contract, the first wholesale 25 kilobar gold contract would be offered globally in October 2014. A Consortium comprising IE Singapore, World Gold Council, Singapore Exchange, and Singapore Bullion Market Association (SBMA) introduced centralised trading and clearing of a physically delivered gold contract in Singapore. The series of six daily contracts gives buyers physical access to competitively priced kilobars. Singapore’s position as the trading hub for ASEAN was further enhanced by the launch of the ICE One-Kilo Gold Futures on 17 November 2015.

During the launch, the Consortium considered itself ahead of all other industry players looking at the same proposition of modernising the spot gold market in light of the fierce regulatory headwind pushing the OTC trade into exchanges. The wholesale kilobar gold contract did not take off as intended. The contract was made dormant in March 2018, only to review the possibility of reviving it when the regulatory and market conditions change, the same happen to the ICE One-Kilo Gold Futures the following year.

Post analysis identified two critical initial issues, first, the lack of trading related to the size of the contract of 25 kilos; secondly the inability to select brands of kilobar/differential in premium pricing. The determining factor that led to its closure, as cited by the members, was the lack of efficiency compared to the OTC trade and the inertia to change among traders, leading to the view that efforts to change the other two issues may be insufficient.

A new era

In 2016, with the ambition to build Singapore as a precious metals trading hub, IE Singapore funded the formalisation of the SBMA and helped to raise its profile under the Local Enterprise and Association Development (LEAD) program.

Since 2017, SBMA has organised its annual Asia Pacific Precious Metals Conference (APPMC), a platform for the precious metals community to raise and discuss issues related to the Asia Pacific precious metals market. APPMC aims to provide networking opportunities for the bullion, jewellery and mining sector from the region and the world. Delegates could also learn more about new markets and meet new customers and suppliers from ASEAN and Asia through the conference. SBMA also publishes its quarterly newsletter Crucible to encourage stronger ties among participants in the industry and create new growth opportunities.

Originally, SBMA was established in 1993 to represent key stakeholders from the precious metals industry, including bullion banks, exchanges, refineries, bullion merchants and secure logistics companies to dialogue with the authorities related to GST exemption on gold trading activities and products, it remained focused on social activities until it was formalised in 2016.

SBMA now provides market knowledge and advice to relevant ministries and government agencies both in Singapore and ASEAN; industry stakeholders; bullion banks; and other business entities related to the bullion business. We are enabler and super connector to our members in developing the ASEAN countries bullion business.

Jewellery market

The Singapore jewellery market is a developed and matured consumption market, with no manufacturing facilities except some workshops doing some bespoke pieces with designers. But Singapore has the advantage of being able to source the latest jewellery designs from manufacturing centres in China, Malaysia, and Indonesia as well as Italy and Turkey. Major players, including Poh Heng, Aspial, SK Jewellery Group and more, each have different types of shops established under different brands to cater to different categories of customers. Middle-class consumers typically purchase mid-priced products from regular jewellery stores or goldsmiths, as well as through online platforms. Like other Asian gold jewellery buyers, both mass market and high-end buyers do not only purchase gold jewellery as accessories but also look for investment value in the jewellery that they choose to buy. Without a doubt, both classes are equally important to the jewellery market in Singapore.

Retail investment

Retail investors look for small bars and coins or gold saving account to gain exposure to gold investment. UOB is the key provider of gold savings accounts, as well as small and kilo gold bars to retail investors. Some gold jewellery outlets also sell small bars and coins as well and they provide more convenience than banks because they have longer service hours and are easily accessible across the country. In recent years, with the advance of online service providers, retail investors, particularly the younger and tech savvy, have been patronising key players like GoldSilver Central, Silver Bullion, Bullion Star; while high net worth individuals also deal with Global Precious Metals and J. Rotbart & Co., which also offer storage solutions as well.

Regulatory bodies

- Enterprise Singapore (ESG) – Spot Commodity Trading

- Monetary Authority of Singapore (MAS) – Exchange trade and derivative trade

- Inland Revenue Authority of Singapore (IRAS) – GST

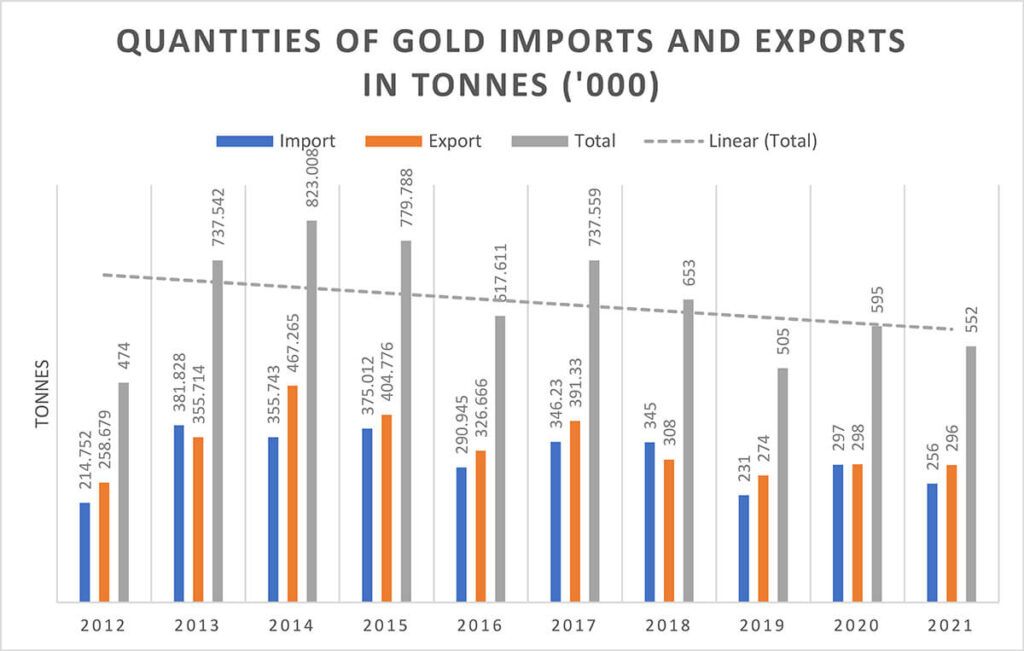

Gold Import and Export Statistics

Table 1: Key Figures

| Non-Monetary Gold HS 71081300 & HS 71081200 in Tonne | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | |

| Import | 215 | 382 | 356 | 375 | 291 | 346 | 345 | 231 | 297 | 256 |

| Export | 259 | 356 | 467 | 405 | 327 | 391 | 308 | 274 | 298 | 296 |

| Total | 474 | 738 | 823 | 780 | 618 | 738 | 653 | 505 | 595 | 552 |

HS Code: HS71081210: Non-monetary gold in lumps ingots or cast bars HS71081290: Non-monetary gold in other unwrought forms HS71081300: Non-monetary gold in semi-manufactured forms